BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material

BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material: We provide to all the students BCom 1st, 2nd, and 3rd Year notes Study material, question answers, sample papers, mock test papers, and pdf. At gurujistudy.com you can easily get all these study materials and notes for free. Here in this post, we are happy to provide you with BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material.

BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material

(Audit Programme)

“Modern Techniques require a new approach to the practical aspect of the auditor’s work.” -Taylor and Perry

PRINCIPLES VS TECHNIQUES

Audit principles are the basic rules and involve all those procedures which are completed during the course of the examination. Techniques are the devices which are adopted in applying these principles. For example, purchases of raw materials is always a revenue item as a matter of principle. The receipt of vouchers such as order, invoice, etc., and verification of their existence is a process and to check their correctness and authenticity becomes a technique ultimately.

Techniques of Audit

It is established that techniques of the audit are the devices or methods through which an auditor proceeds in his work to obtain evidential matter. Some of such techniques are given below:

(i) Vouching. An auditor examines documentary evidence relating to the recording of transactions in support and thus, checks the authenticity of such records. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

(ii) Confirming. It is a technique with an auditor to contact responsible officials through interview and to open communication with the outside parties for ensuring that the transactions are authentic, valid and accurate.

(iii) Reconciling. The differences in figures are reconciled and causes for their existence are brought to light.

(iv) Analysing. The device or process of segregating any accounting facts or is known as analysing.

(v) Testing. This technique is applied to examine a large number of transactions by selecting actual representative data with accuracy as far as possible.

(vi) Physical Examination. To examine the actual existence of an item, personal inspection by an auditor becomes absolutely essential.

(vii) Scanning. This implies a critical study or appraisal of the characteristics of data.

(viii) Verification of Posting. To establish propriety and consistency of different entries, the records in the books from one source to another can be verified. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

(ix) Footing. To test accuracy of total, the columns of different accounting figures can be added.

(x) Extension Verification. It implies the multiplication of two or more amounts to test the accuracy of the total.

PREPARATION BEFORE AUDIT

How to prepare and proceed with the audit is another pertinent question to be examined. How much time should be devoted by an auditor to auditing the accounts of a business concern will depend entirely upon the circumstances of a particular case and the training, experience and knowledge of the auditor. This much is certain that the auditor must prepare well before he actually conducts an audit.

His preparation will be decided by the scope of work assigned to him and the method in which he will proceed. To examine the issue, we may proceed step by step. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

1. Scope of Work to be Determined

The scope of work will depend upon the terms of the agreement entered into between him and his client, or upon the conditions laid by the appointment letter issued to him. It is true that if the auditor is to examine the accounts of a joint-stock company, he has to proceed and prepare in accordance with the provisions of the Companies Act and as such, in such a case, the question of any agreement does not arise. But in other cases, it is the client who decides the extent of the work which the auditor has to perform with regard to the checking of accounts. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

Before determining exactly the scope of his duties, the auditor should discuss the nature, purpose, etc., of the audit that he has to conduct. If certain limitations have been placed on his duties, he should thoroughly know them and note them carefully in his Audit Note Book. This is very essential. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

2. Knowledge of Business

Next, the auditor should try to acquire full knowledge of the business and its affairs. For this, he should proceed with the scrutiny of some important documents and procedures:

(i) He should go through the rules and regulations which make the business in question run, e.g., Memorandum of Association, Articles of Association, etc., in case of a joint-stock company and partnership agreement in case of a partnership firm. The study of such basic and guiding documents can make him familiar with the working of a business and hence, the thorough knowledge and study of these rules are highly imperative for the auditor. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

(ii) Further, he should examine the method of maintaining accounts. It should be remembered that different types of business houses, e.g., banks, and insurance companies. joint-stock companies, cinema houses, gas companies, educational institutions, etc., use different systems of keeping books of accounts. Hence, the auditor should make himself familiar with the nature of business so that he can satisfy himself with regard to the accounting system being satisfactory or otherwise.

(iii) Next, he should ask for a list of books of accounts maintained and also the names of clerks who are assigned the role of keeping them from his client. Apart from this, he should obtain the names of the responsible officials who control the various branches of work.

(iv) The auditor should examine the system of an internal check-in operation. The efficacy or otherwise of this system will help him in determining the main lines on which he should conduct the audit. If the system is defective, there are chances of errors and fraud in the books of accounts. A sound system of internal checks can minimize such chances.

(v) Technical details about the business: To make the work of audit more meaningful and effective, the auditor should fully acquaint himself with the technical nature of the transactions recorded. Since no two businesses are alike in nature, he should acquire the necessary knowledge of business affairs. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

(vi) Lastly, it is also advisable for the auditor to go through the Profit & Loss Account and Balance Sheet of the previous year and look into the various objections, if any, raised by the auditor in his previous year’s report. This should especially be done if an auditor is appointed to supersede another auditor. If necessary, the retiring auditor may be contacted.

3. Instructions to the Client

After having acquired up-to-date knowledge of the affairs of a concern, the auditor should ask the client to direct his staff with regard to the following:

(i) The books of accounts should be totalled up and the trial balance and final accounts should be kept ready.

(ii) All the vouchers should be serially arranged and filed.

(iii) The schedules of debtors and creditors should be prepared.

(iv) A list of bad and doubtful debts should be prepared.

(v) Similarly, a schedule of outstanding and prepaid expenses and accrued income should be kept ready.

(vi) Stock-sheet indicating the method of valuation of stock should be drawn up.

(vii) A schedule of investments indicating their cost price and market price should be prepared.

(viii) A certified list of goods returned by different branches, agents and other similar institutions should be made available at the time of audit.

(ix) A statement containing details about the permanent capital expenditure should be kept ready.

(x) Similarly, a list of deferred revenue expenditures should be prepared.

(xi) A list of those documents to which the auditor will have access should be prepared.

(xii) Names and addresses of Managers and Managing directors should be kept ready for submission to the auditor.

4. Preparation by the Auditor

Next, in the series of various steps to be taken by the auditor before he actually begins the audit of the business of his client is the preparation that he makes for himself. The following are some of the important aspects of his preparation:

(i) Distribution of Work

The auditor should distribute the work and assign duties among his subordinates according to their qualifications, experience and training. They can be of two types—senior and junior. It is very necessary that the senior clerks should be assigned such duties as relate to difficult and technical work and the junior ones in his staff should be given simple type of work.

But, after all, it is the auditor who has to certify the accounts as correct and, as such, he is ultimately responsible for all the actions of his subordinates. Hence, the preparation of an auditor at this stage is of special significance.

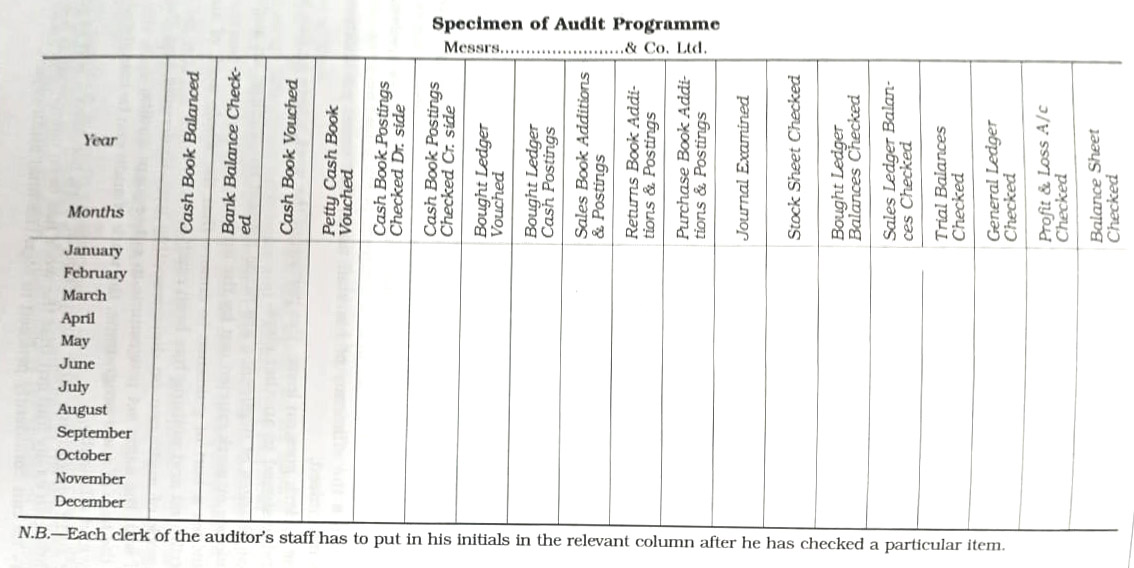

(ii) Audit Programme

Technically speaking, an audit programme is the auditor’s plan of action. It presents an outline of procedures to be followed to support an opinion on the financial statements The primary basis of preparing an audit programme is the system of internal check or control and since no two internal control systems can be exactly alike, an audit programme will also vary among clients and business firms.

An auditor, therefore, will have to keep in mind a basic programme which he would modify to fit the special circumstances of each case. Modifications to the basic plan of action are based on the weaknesses inherent in the system of internal checks or control prevailing in a particular business. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

“An audit programme is a detailed plan of the audit work to be performed, specifying e procedures to be followed in the verification of each item in the financial statements and giving the estimated time required.” –Prof. Meigs

An audit programme is a written scheme prepared by the auditor to distribute work to be followed during an audit. The preparation of such a programme involves mainly three things:

(i) How much work is to be done?

(ii) Who is going to do a particular portion of the work?

(iii) What is the duration of time by which the work is to be finished?

Thus, the idea Implied in the preparation of an audit programme is to ensure to the auditor has a complete grip over his staff including his juniors and seniors, the procedures to be followed and the portions of work actually to be performed by each of them and by himself. The work involved in the preparation of the audit programme is usually done by a senior clerk in his staff.

As has already been indicated earlier, the division of work connected with the audit of the business of the client should be based on one principle, le., work to be distributed according to the qualifications, experience and training of clerks, juniors and seniors. An audit programme makes each of them certain about the specific task one has to perform, i.e., everyone knows what he has to do and by what date each item is to be completed. Usually, such a programme is prepared well in advance, though, of course, sometimes it may be allowed to grow as the work progresses. But the first practice is definitely more useful.

Advantages of the Audit Programme

- The audit programme is prepared to locate exactly the responsibility of every clerk in the auditor’s staff. Thus, each one of them gets work according to his capacity. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

- The auditor can know about the progress of the work done by his staff.

- Since the programme takes into consideration all the details involved in the work to be followed during an audit, no portion of the work is left from checking. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

- It increases the efficiency of his staff as in that case, the possibility of errors and negligence is minimized.

- In case a clerk goes on leave, the portion of the work where he has left can easily be located and assigned to another clerk.

- In case charges of negligence are made against the auditor, an audit programme serves as evidence of work carried out by the auditor.

- It provides a sort of guidance to ensure that the whole work of the audit has been properly distributed and nothing has been omitted.

- The work of audit can be done smoothly with uniformity and the auditor can proceed well with the same set programme in subsequent audits.

- With the help of an audit programme, the work of audit can be completed in time quite methodically and efficiently.

- The audit programme after the completion of work becomes a sort of progress chart and the auditor can easily find out that the work has been completed as per his plan and with its help, he can confidently proceed to sign the final audit report.

Disadvantages of the Audit Programme

The following are the disadvantages of the audit programme:

- A written audit programme leaves no scope for creativity on the part of the start carrying it out with the result that audit work more often became mechanical in nature. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

- As the requirements of every company vary a different audit programme is needed for different companies and a uniform audit programme may not suit all companies.

- Inefficient audit staff may try to hide their incompetence behind rigid/fixed audit programme giving pleas that no specific instructions were issued to them. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

- In an ever-changing dynamic environment, constant amendments and updations are required in the audit programme every year to meet the changing needs of client companies.

Hence, to guard against the disadvantages, it is usually suggested that an audit programme should be divided into two parts, viz.,

(i) Work common to all types of audit; and

(ii) Work relating to a particular audit.

This will, therefore, leave some scope for modification to be made in the audit programme whenever necessary. It is well said that “an audit programme to be serviceable must be elastic.” A flexible programme can provide an opportunity for clerks to exercise their intelligence and initiative. The programme should be prepared and made up-to-date in accordance with the nature and character of a business.

Other Precautions

- The audit programme should be amended or revised in accordance with the internal control system to be reviewed from time to time and from firm to firm. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

- It should also be revised by the auditor if a new system or a new line of action has been adopted by his client.

- The junior assistants should be consulted while preparing the audit programme. They should be given adequate encouragement.

- A rigid and stereotyped programme should be avoided.

- While using the audit programme by juniors or audit assistants, they should feel that they have actually some discretion in practice.

(iii) Audit Files

An auditor is often simultaneously occupied with a number of audits. Moreover, he is mostly bound to his office in order to control and coordinate the activities of his staff working at different places. Hence, it is necessary for him to maintain a record of each audit for ready reference. Such record is maintained in files, called audit files.

Thus, there may be two types of audit files: (i) permanent audit file, and (ii) current audit file. The permanent audit file contains the following matters:

- The rules govern the company or the organization under audit such as Memorandum and Articles of Association in the case of a company and partnership deed in the case of a partnership firm.

- Copies of minutes and extracts of agreements which are entered into between the client and others for rendering/obtaining services.

- A brief description of the business, its nature, address, area of operation, etc.

- Particulars about the organization of the business along with a list of officials, branches and departments under their charge.

- Copy of instructions, if any, issued to the staff and of relevance to the auditor.

- List of books and registers and names of persons dealing with them.

- Copies of audited financial statements of previous years.

The Current Audit File contains the following matters:

- The audit programme was duly amended and modified in accordance with the system of internal control in use.

- Internal control questionnaires.

- Flow chart covering the time budget.

- All relevant notes are properly filed and indexed.

- Bank and petty cash reconciliations.

- Brief notes for discussion with the client before completion of the work of audit.

- Weaknesses are inherent in the system of internal control.

- The draft final accounts and Balance Sheet and their completed copies.

Advantages

- It assists in the preparation of an audit plan which paves a way for subsequent audit engagements.

- It is a useful file for the use of an auditor who depends on it for forming an opinion about the matters to be included in his report.

- It is a ready reference for an auditor and provides different materials to be used in the fieldwork in audit engagement.

- It provides information to an auditor who is asked by the client to suggest improvements in business operations and the system of accounting.

- It maximises efficiency in auditing procedures.

(iv) Audit Note-Book

The audit notebook is maintained by the audit clerk. He keeps there a record of his observations during the course of any audit work. He also notes down the important points and enquiries that he has to refer to the officials of his client or to discuss with his senior or the auditor himself. Thus, the use of this book has become important to keep an exhaustive record of enquiries made, replies received thereto, correspondence, etc. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

Contents of an Audit Note-Book

- Technical details about a business;

- Queries for which explanations and information have to be demanded, e.g., missing vouchers and invoices;

- Fraud and errors found in the books during the course of the audit;

- Details which are to be included in the audit report;

- Notes regarding the system of maintaining accounts;

- Information to be needed in future:

- Names of officials who certify bad debts, depreciation, etc;

- Record all important correspondence;

- Totals of important ledger accounts:

- Progress of audit work;

- Record of suggestions made by the audit staff.

Advantages

- The auditor is enabled to record important points which arise during the course of his audit lest he might forget these points.

- He can produce this book as documentary evidence in a suit filed against him for negligence or misfeasance.

- A notebook makes the work of an audit convenient as all the important details about the audit can be recorded in this book and, as such any change in the staff of the auditor does not disturb or dislocate the work of the audit.

- Such a book can help in making an assessment of the knowledge, efficiency and work of audit clerks,

- It makes the procedures of subsequent audits easier.

- It provides a key to evaluating the efficiency of the audit staff.

Thus, the proper use of this book can be of great value for subsequent audits of the concern or of other businesses. Actually, this serves as a guide to the audit staff. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

Disadvantages

- It develops a fault-finding attitude in the minds of the audit staff.

- It places too much reliance on the staff of the client for its preparation.

- If an audit notebook is prepared negligently, the auditor can use it as evidence of negligence in the courts of law.

- Very often, it creates misunderstanding between the client’s staff and the audit staff.

(v) Audit Evidence

Audit evidence has got wide coverage and has a direct impact on the mind of an auditor so as to enable him to judge the truthfulness of prepositions brought before him for scrutiny and analysis. It is through evidence that the auditor can form an opinion about the financial affairs,

Several evidences are to be collected for each assertion made in the financial statement. Such assertions are varied and are of various types meaning thereby that their nature differs under different circumstances.

Such evidence is not only documentary evidence but may be in the form of personal enquiries, observations, verifications and inspections. There may be two important considerations for planning the method of obtaining audit evidence which are:

(1) Types of evidence to be made available to the auditors:

(2) Means of getting such evidence.

It is to be noted that the nature of evidences depends entirely upon the circumstances of individual cases. In the absence of a well-knit internal control system, the need for proper evidences becomes more imperative.

Kinds of Types of Audit Evidences

1. Physical verification or inspection: Physical inspection or verification is the best rather than the most effective evidence through which physical inspection of cash, tangible assets, petty cash etc, can be easily made and their existence with the business can be ensured.

2. Statement by independent third parties: Statement made by a competent third party is one of the strongest types of audit evidence. Such parties may be debtors, creditors, solicitors of the company. Obviously, the amount of debtors can be confirmed by obtaining statements from debtors. Such statements may be written or oral. (BCom Preparation Before And Procedure of Audit Study Material)

3. Authoritative documents: Documentary evidence is usually more reliable than oral representations. The various documentary evidences are purchase invoices, copies of sales invoices, petty cash vouchers, contract deeds, receipts, receipts given by payees, debit and credit notes minutes of meetings etc. These authoritative documents are considered to be the main sources of evidences.

Some documents prepared from outside the organisation may be considered reliable evidences but those prepared inside the organisation are not always reliable. However, the auditor should be alert and should exercise reasonable care and skill before considering those documents for the purpose of audit. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

4. Statements by officers and employees of the company under examination: The statements given by officers and employees may be formal or informal. The auditor should show not place full reliance on the statements given by the officers and employees of the organisation under audit. The employees who prepare accounts may conceal some material facts. That auditor in case of suspicion may call for explanation and clarification from officers of the organisation.

5. Calculation performed by the Auditor: The calculation performed by the auditor forms a part of the evidence and in order to verify the arithmetical accuracy of the calculation that appears in the accounts he may be required to recalculate it. These re-calculated figures must be recorded and may act as evidence when occasions warrant.

6. Satisfactory Internal Control Procedures: It is an important duty of the auditor to see whether the internal control procedure is functioning satisfactorily or not. If not, such a system cannot be considered as an evidence of reliability. How far this system will be reliable will depend upon the skill of the auditor who can appraise or evaluate the system for his work.

7. Subsequent actions by the company under examination and by others: The subsequent action by the company under examination constitutes a type of evidence in the sense that the statement of fact by the company as to the events subsequent to the balance sheet date may materially affect the financial statement and auditor’s report. This is because the actual audit work starts after the end of the financial year. Thus the statement of fact by the high officials of the company acts as evidence which can be relied on by the auditor with “little fear of going astray”. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

8. Subsidiary or Detailed Records with an significant indication of irregularity: Subsidiary or detailed records may be considered another type of evidence through which certain amount of reliability relating to the different figures may be obtained. Records like store ledgers if maintained properly and having no indication of irregularity may appear to be supporting evidence to the auditor.

9. Inter-relationship with other data: Sometimes accounting data can be interrelated, with other data. The result arising out of the reconciliation of two figures may be taken as evidence in support of the transactions.

It is for the auditor to collect evidences with special care and knowledge. It is for him to make out the real significance of accounting data and evolve ways and means to prove that evidence is vital so far as the audit procedure is concerned.

(vi) Audit Working Papers

Audit working papers are those papers and documents which consist of details about accounts which are under audit. The auditor notes down certain important facts and details about accounts in these papers. The objects of an auditor’s working papers are to control the current year’s audit and to provide a base for the audit of the following year. It also aims at providing detailed information about the accounts and business of the client. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

The use of these papers is quite important as it helps the auditor to make a reference to these papers whenever needed while going over the accounts of his client. Such details may be the following:

- Schedules of debtors and creditors;

- Certificates of officials in regard to such important matters as bad debts, valuation of stock, unpaid expenses, accrued income, etc.;

- Certificates issued by the banks in regard to the bank balance of the client on a certain date, safe custody of documents, etc.;

- Correspondence between the auditor and the debtors, creditors, etc. of the client.

- Rough trial balance;

- Important extracts from the minute books:

- Particulars of investment:

- Draft final accounts;

- A copy of the auditor’s book.

Purposes of Working Papers

- These papers represent the volume of work which has been performed by the auditor and his staff and hence, it becomes quite easy to draft and prepare a detailed audit report.

- The various minute details and aspects of the audit report can be well substantiated on the basis of findings summarized in the report.

- The working papers become an asset for the auditor on the occasions when he has to defend himself against the charges of negligence etc., levelled against him. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

- The auditor can coordinate and organize the work of audit clerks with the help of working papers.

- The auditor’s detailed advice to his client in regard to improving the system of internal checks and efficiency of the accounting system can be available to the client.

- The working papers act as a guide to the auditor in subsequent examinations.

Audit working papers should be complete and concise and contain all the relevant information in regard to accounts and audits. They should be properly arranged and preserved for future reference. The auditors use these papers in drafting their final audit reports and hence, they become valuable for future audits too. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

Characteristics of Good Working Papers

- They should be complete in all respects. They should clearly reflect full information and should not include any superfluous material. Only essential data should be contained therein so that they may be of utmost utility.

- They should be properly organized and arranged. The proper arrangement of these papers will also make them easily understandable to those concerned. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

- The working papers must contain accurate information.

- There must be clarity in thought and expression. The clarity of ideas contained in the working papers makes them self-explanatory and easily understandable. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

- The relevant details should always be kept in the working papers.

- The audit working paper files should be properly preserved and filed.

Ownership of Working Papers, etc.

The working papers are highly confidential papers and, therefore, must be kept in safe custody. As for the ownership of these papers, there has arisen a lot of controversy whether these papers belong to the client or to the auditor. The former claims that since the auditor is his agent, he has no lien on these papers. On the contrary, the auditor establishes his claim on them on the ground that they are his property as he has collected le information for the purpose of discharging his audit duties.

Actually, these papers come to the rescue of the auditor at a time when a suit has been filed against him by his client for negligence or any other charge. These papers serve as evidence for the auditor to defend himself. Therefore, auditor should be considered as the rightful custodian of working paper. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

In the cases of Sockockcockinsky vs. Bright Grahm and Co. (1938) in England and Chantrey Martin & Co. vs. Martin (London, 1953), the question was whether the auditors had a right to retain the working papers as if it were their own property even after the payment of the audit fee. It was held that the working papers belonged to the auditor and not to the client.

PROCEDURE OF AUDIT

How to proceed with the audit is another important issue. No hard and fast method of audit can be laid down but it can be said that the auditor with his prudence, experience and tact will decide himself as to how he will proceed with the work during audit and what method he will actually adopt. It is true that the success of his mission will absolutely depend upon his own skill.

1. Adoption of Distinctive Ticks

The auditor should use distinctive ticks of various colours while auditing the books of accounts of a business. But successful use of ticks involves a lot of care to be taken by the auditor. The following are some of the safeguards against improper use of such ticks: (i) He should use different types of ticks for different purposes, e.g., vouching, postings, additions, carry-forwards, etc.

(ii) He should issue clear instructions to the members of his staff that the use of these different ticks should not be made known to the clerks of his client. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

(iii) While using ticks the auditor should have the pencils and inks of different colours in his control.

(iv) Vouching should be entrusted to two clerks like this:

(a) The senior clerk should check the voucher and call out the amount given in it, and

(b) The junior clerk should compare the amount and place a tick against the item in the Cash Book.

Some Other Important considerations

(i) As far as possible, the work connected with the checking of a book should be finished in one sitting. If it is not possible, its important totals, balances, etc., should be noted in the audit notebook.

(ii) In case of continuous audit, the work of audit should be done upto a particular date. Pencil figures should not be accepted.

(iii) The audit clerk is not expected to balance books. If he does so, he works as an accountant and not as an auditor. Generally, in small business concerns, where there is no accountant, the auditor has to balance the books.

2. Routine Checking

Whatever may be the size, constitution, and nature of activities and transactions of a business, there are certain records and books which are common to all types of business organizations. The checking of such common records and books which is carried on by the auditor as a matter of routine is known as routine checking in auditing. Routine checking involves normally four types of functions:

(i) Checking of casts, subcastes, carry-forwards and other calculations in the books of original entry:

(ii) Checking of postings into the ledger:

(iii) Checking of casts and balances of various accounts in the ledger; and

(iv) Checking of transfer of balances from the ledger to the trial balance.

Thus, routine checking can verify the arithmetical accuracy of the entries made in the books of accounts. It can help in checking castings and postings and, as such, can ensure that no alterations are made in the figures after they have been checked and ticked accordingly.

Advantages

(i) The books of original entry can be thoroughly checked and the errors and fraud can be easily detected.

(ii) Postings (i.e., matters taken from records made in the books of original entry to the ledger) can be checked.

(iii) The checking of castings and postings done in routine checking is the very basis upon which the final results of the audit depend. Hence, it helps in the checking of final accounts ultimately.

(iv) It reveals the errors and fraud of a simple nature and helps in the verification of the arithmetical accuracy of the entries.

Disadvantages

(i) Routine checking is practically a mechanical process and hence, it can cause monotony to those who are entrusted with this task.

(ii) Only minor cases of fraud can be detected by routine checking. Major items of fraud cannot be brought to light.

(iii) It is difficult to trace out compensating errors and errors of principle.

(iv) Routine checking is not always considered important in the audit of a business where self-balancing system is used.

3. Test Checking (or Selective Verification)

Just to reduce the time cost involved in the audit of a big manufacturing concern in which there are large number of transactions, an auditor usually adopts the technique of test checking.

Test checking is a substitute for detailed checking. Here, an auditor, through a process of sampling, selects a few items and if they are found correct, he presumes that the remaining entries would also be correct likewise. Thus, test checking is based on a simple theme that “If a representative number of transactions, so selected at random by the auditor for test checking, is found to be correct, the remaining ones would also be correct.”

Thus, the whole system of test checking implies selecting and checking only a few selected transactions so as to enable the auditor to form his final judgment as to the whole set of transactions.

As stated above, in applying ‘test check’, the selection of transactions is made by the auditor at random and no specific principles are followed in it. The choice for adoption of testing methods is fully dependent on the discretion and judgment of the auditor who will depend on the situation of individual cases. The use of test checking is, however, dependent upon the system of an internal check-in operation.

If this system is satisfactory. test checking can be of immense help to the auditor. But it should be kept in mind that if the system is reliable and test check is applied but mistakes are detected, a thorough checking of books would provide an answer. Thus, given an efficient system of internal check-in operation, test checking can reduce the volume of work involved in audits.

Test checking should be applied and carried out intelligently and carefully, otherwise. it may lead to dangerous consequences. But much will depend on the system of internal check and the intelligence of the auditor.

Safeguards for the Application of Test Checking

(i) As far as possible, representative or sample transactions should be selected from every book or ledger covering the whole of the period under audit. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

(ii) The selection of transactions should be distributed in such a way that the work of almost all the clerks of the client is checked.

(iii) The selection of items should be made at random.

(iv) The entries pertaining to the first and the last months of year should be thoroughly checked as fraudulent manipulations are usually made during these months. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

(v) Cash Book and Pass Book should be thoroughly checked.

(vi) No consultation should be made with the staff of the client when a selection of transactions for test checking is made by the auditor. This is absolutely his job and he should do it with perfect secrecy.

It is to be noted that there are no universally accepted percentage tables or rules for selecting audit sample which is applicable to each type of test. However, the use of test checking or audit sampling provides results which are the same by pure coincidence as would have been obtained by 100 per cent examination of the various transactions. However, statistical sampling is always preferable in the conduct of an audit to arbitrary sampling. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

Advantages

(i) Test checking saves time and energy.

(ii) If the selection of transactions is done intelligently, test checking is useful and purposive.

(iii) It can help the auditor to arrive at a definite conclusion in regard to the true and fair view of the state of affairs of the concern.

(iv) It helps in reducing the cost of audits.

Disadvantages

(i) All errors and fraud may not be detected.

(ii) The staff of the client may become careless because they know that their work will not be checked in detail.

(iii) There may be difficulty in determining the sample size and if the sample is not representative it may lead to misleading results.

(iv) It is of no use if proper and effective systems of checks and controls are not being adopted in business.

(v) It is unsuitable for small business houses.

4. Audit in Depth

Audit in-depth implies a detailed and step-by-step examination of transactions through the processes of the activity from origin to conclusion. In an audit in-depth, comprehensive checking is involved and selected transactions are examined after tracing all the links from beginning to end. (BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material)

The main objective for such a checking is to complete the audit of accounts in a shorter interval and thus, he can maintain the time target in his work. One of the main advantages of selective verifications is to enable an auditor to carry out audit in depth of the selected transactions. Such a procedure can be adopted by an auditor where there is an effective system of internal checks in the business.

As an example, if purchase of a costly machinery is to be checked and as such, purchase is subjected to audit in depth, the following steps will be taken by an auditor:

- to see the minutes of the Directors Meeting to examine whether the purchase of the machine has been authorised or not.

- to inspect the copy of purchase order sent for the purchase of the machinery.

- to check and inspect the machinery purchased.

- to verify the amount paid to the seller.

- to verify the expenses incurred for the installation of machinery.

- to examine the entries made in the Books of Accounts and Plant Register.

This shows that in an audit in depth, the auditor reviews all the accounting and operational aspects of transactions from the beginning to the end. Thus, he can take an overall view of the transaction and evaluates the procedures through selected transactions.

BCom 3rd Year Preparation Before And Procedure of Audit Notes Study Material

Bcom 3rd Year Sample Model Practice Mock Test Question Answer Papers